Material roots, the end of hegemony, the suppression of finance by nature

Environmental breakdown portends the end of hegemony in the world economy, and, with it, the end of the supra-secular decline in real interest rates.

Boats stranded at David's Marina on the Rio Negro, Manaus, Brazil on Oct 16, 2023. River water levels hit their lowest point in at least 121 years. Credit: Bruno Kelly/Reuters

Back, after a significant pause, to publishing here. I’ve been using the space to try and organise some notes around the ongoing/neverending book project, for which it’s been useful – it’s helpful to have an audience of some sort when writing, since it forces a bit of organisation on my thinking, and feedback is very much appreciated. It does mean that what I publish tends to be a bit scattered and ad hoc but I’m hoping the various subscribers can bear with me (and with the peculiar endnoting that’s happened below.)

What follows started as some notes for a section in the book, that then spiralled off somewhat into a consideration of hegemony and finance, referencing (inevitably) Arrighi and Braudel. I’ve been particularly struck by the work on long-run real interest rates, for all the methodological difficulties it presents; the “supra-secular” decline is too clear to be easily dismissed, and needs some form of explanation.

Growth as the key to reformism

Consistent growth itself, as the revisionist work of economic historians has shown, tended only to become embedded at a national level (rather than being a feature of specific sectors and regions) in industrialising economies much later than was previously assumed, in the latter half of the nineteenth century. Consistent rises in working class living standards – certainly beyond a comparatively privileged layer – only really emerge after this mid-century point.[i]

The concomitant development of reformism in the socialist movement required, as a fundamental, an alliance with the state – since what other agency could be reliably found to implement reforms? The breach with anti-state anarchism in the early workers’ movement, following the collapse of the First International, was never healed – anarchism remained as the minority, critical current relative to the great majority of the labour and socialist movements. But that alliance with the state in turn required the development of state capacity: not only in the sense of the reach of the state, in developing its bureaucratic reach and extending the scope of its functions more widely across social life, but also in the expansion of the economy on which the state rested. Economic growth provided the basis for expanded private provision of goods and services, creating the base for near-continual improvements in living standards, but also provided the wherewithal for extended public provision without intruding on the needs of private capital too closely.

Over the next century, the development of the socialist and social democratic parties, and their associated labour movements, tended to shift to an increasing focus on shares in expanded prosperity as the primary goal of economic policy. Growth became the pinnacle of economic policy once the tools have been developed to allow its measurement and, with less accuracy, regulation – primarily the creation of Gross Domestic Product and the subsequent standardisation of national accounting, combined with the refinement of Keynes’ General Theory insights. In the immediate post-WW2 period, all of this came together to produce a seeming “Golden Age” (in Eric Hobsbawm’s phrase) for the developed world: fast growth, rising living standards, and an expansion of the welfare state, based on the exceptional extension and deepening of the “cheap nature” regime (notably in the form of cheap oil), and the coincidence of globally stable environmental conditions. The “rescue” of the European nation-states, post-war, depended on the stability rapid (and broadly-distributed) economic growth could provide;[ii] later editions of capitalist modernisation, notably across East Asia, delivered typically faster rates of growth but, in the neoliberal period, with less concern for its equitable distribution.

The post-WW2 alliance, in the West before 1989 and globally thereafter, was between the capitalist state and national capital, with labour very much as a subordinate partner or (typically, in the neoliberal period) not even that. Its subordinate status could be justified and sustained on the basis of the promise of continued growth. Neoliberalism extended the zone of waged labour, the response to crisis of the 1970s involving both the mass expansion of the waged work of women,[iii] and (after 1989) the incorporation of many millions of newly-urbanised workers into the global labour system.[iv]

The difficulty we face, collectively, is that natural disorder of the kind presented by covid is only likely to get worse as the stable environment shifts away from us, in both directions: upsetting both the rhythms of production and disrupting the conditions under which social reproduction can occur. There is a lesser order of this problem in the Western economies: economic models, and economic policy, developed for a world in which the environment itself was taken as read are no longer fit for a world in which that assumption does not apply. The kind of permanent instability and volatility of the background conditions on which human economic activity depends do not feature in standard models of, for example, the macroeconomy; and for the period of time that economics has existed as a field of human knowledge, this has been a reasonable assumption to make. Costs and conditions of production would be stable over time, subject only to the fundamental forces of either declining marginal productivity, or increasing returns to knowledge.

War, sovereignty and disease

But if the mechanism of stable growth has broken down, so, too, is the regime of international relations. Crucially, this is particularly weak in international public health. At the turn of the millennium, technological developments – both in terms of communication and scientific progress in managing disease itself – had allowed the belief to form that a new kind of international public health regime had begun to emerge, one free from the earlier requirements of national sovereignty. The relative speed and effectiveness with which the SARS outbreak in 2003 was dealt with was hailed in subsequent years as a triumph of “post-Westphalian” global public health policy: of a shift away from the “Westphalian” model of state-centred public health action with non-intervention inside states a guiding principle, towards a new, globalised “post-Westphalian” model of health action in which agreed standards were applied across states.[v]

This, obviously, turned out to be hubristic. The breakdown of even the usual public health cooperation between nations has been only too evident, involving disputes over the allocation of vaccines in scarce supply and, extraordinarily, the removal of US public funding from the sole body charged with guarding international public health. Compared to the very robust and often mercilessly efficient guardians of the financial and economic system- challenged as they have been in recent decades - international public health institutions seems shockingly weak by comparison. And yet it is international public health cooperation that will be essential in a world increasingly beset by disease.

One instance of this breakdown in cooperation is the sheer spread of different policy options adopted by different countries. The neoliberal playbook gave a robust set of policy prescriptions and guidelines for governments, a theoretical justification for them, typically hinging on various claims about globalisation, and the institutional means for their enforcement, from the bond markets to the International Monetary Fund to the World Trade Organisation. The result was a striking convergence of policy: the pensée unique that was dominated how policy was supposed to be done, at least until the 2008 crisis.[vi]

The World Health Organisation was (and is) dramatically underfunded, with a budget of just $4.4bn in 2020, “less than that of a single big city hospital”.[vii] Beset by internal rivalries and, as covid spectacularly revealed, subject to the new dynamics of emerging Great Power competition between the US, China, and other states, the WHO was in no serious position to impose itself on anyone. Its plaintive appeals for the ending of intellectual property protections, even when backed by some of the world’s most populous states, fell on deaf or, at best, condescending ears in the Global North. Its attempts to navigate between the desires of the Chinese government to impose strict controls over the reporting and investigation of the covid outbreak, and the demands of the rest of the world for openness, resulted in some alarming back-and-forth on questions of policy through the first years of the pandemic.

In this, the WHO parallels other weak global structures that aim to achieve global public goods, most notably those associated with climate change. Whilst there have been important steps here, the pace of global transition into low carbon energy systems is far slower than would be ideal: neither the much-heralded Paris Agreement – a genuine breakthrough – nor the various scientific authorities charged with overseeing the disaster have the authority to impose themselves on a world-system facing increasing disorder. It remains the case that the annual COP process, since Paris in 2015, is the closest that the global economy has to any form of genuinely global, multilateral cooperation and regulation; but it is also the case that its real powers and capacities remain incredibly weak compared to the scale of the challenge.

The end of sovereignty

The central dilemma is this. As we move from a world where humanity can impose a direction on the planet, to one in which nature itself is imposing on us, the weakness of the structures we have in place to manage and resolve the conflicts that are inherent to a system of competing states and capitals will become more apparent. The global structures through which hegemony has operated over the last few centuries, through financial systems and international economic organisations, from Genoese merchant families to the World Bank, IMF and WTO,[viii] are irreparably weakened by the ecological decay, and no parallel alternative structures have been created – or, most likely can be created – to replace them. A world-system built around the World Health Organisation, assorted climate change agreements, and conflicting regulatory arrangements on data,[ix] rather than the financial and economic institutions of old is a world-system in a state of permanent, and potentially worsening, weakness.

Attempts to reassert versions of sovereignty against the disorder – what Geoff Mann and Joel Wainwright have usefully topologized as “Climate Mao” and “Climate Leviathan”, depending on the claims the ecologically-focused sovereign makes about its own legitimacy[x] – are likely to flounder precisely because no sovereign has the reach that would provide meaningful control in this way. Attempts to close the gap between sovereign claims and capacities through technology – notably through geoengineering – themselves contain extraordinary risks likely to merely increase the instability and disorder they are intended to counter.[xi] At a national level, whatever impacts on short-run growth investment in digital technologies may provide, the pandemic revealed that digital tech is extraordinarily well-suited to the provision of additional instruments for surveillance and control, national sovereigns integrating with Big Tech. The actual impacts on growth from this investment are more uncertain.[xii]

It will not be possible to escape from this bind, between weak sovereigns and weak growth. Typically, visions of the end of state sovereignty associated with the utopian future of “full communism” (or some similar formulation) depended on the maximum possible expansion of productive capacities.[xiii] Lenin, in the State and Revolution, argues that the state “will be able to wither away completely when…people have become so accustomed to observing the fundamental rules of social intercourse and when their labour has become so productive that they will voluntarily work according to their ability.”[xiv] The “productivist” bias on the left is substantial. But the future ahead of us is one in which sovereignty and productivity are threatened by ecological disorder – not a future where one can substitute for the other.

The end of modernity

The consequences of this shift the locus of collective human agency, from the nation-state and the system of nation-states, towards something more chaotic and uncontrolled, is suggests the opening of a period of profound disorder in human affairs. What Charles Tilly called the “master process” of the modern era, “the creation of a system of national states and the formation of a worldwide capitalist system”,[xv] is significantly challenged: neither the nation-state, as guarantor of domestic security, nor the world-system, as guarantor of external harmony, are likely to function as we have become used to. Fundamental elements of the global economy, including the formation of a hegemonic “world money”[xvi] as an organising point for the formation of global markets, are presently being thrown into substantial question by a combination of war, supply shocks, and a shift in the balance of economic power eastwards.[xvii]

This systemic monetary dislocation is itself an amplification of the post-2008 state-led attempts to rescue national economies as Quantitative Easing was resumed with extreme vengeance in early 2020. But whilst in the immediate aftermath of the 2008 crisis, national central banks and – critically – the Federal Reserve had the capacity to restore good order to national economies and the international system, both the sheer scale of monetary interventions prior to covid – the immense hoards of liquidty that have been built up outside of the immediate control of sovereigns and regulators - and the presence of continuing, and essentially endless, instability mean no part of the monetary system now holds that power. Intervnetions by central banks today are likely to in turn help translate the shortages and disruption of the early Anthropocene into inflationary episodes and credit bubbles at the level of national economies.

The primary manifestation of this will be in the combination of inelastic supplies of essentials (“double inelasticity”: inelastic supplies of goods and services with inelastic demand) with “excess elasticity” in credit and money combine to lean the system as a whole towards higher and more volatile inflation – interspersed with varying financial crises. The notion of expansive monetary sovereignty, as something might be easily and cleanly enjoyed by multiple states looks particularly dubious when even the power and authority of the US dollar is being brought into question.

Previous periods of hegemonic shift were also marked by forms of monetary and price disorder: the “price revolution of the sixteenth century” that accompanied the rise of Genoese financing to is hegemonic position, or, in contrast, the long deflationary period that accompanied the rise of London to its during the nineteenth.[xviii] Giovanni Arrighhi attributes this to the contrast between the ultimate failure of the Spanish Empire to secure its hegemonic position relative to the success of the British, and that the cycles of inflation and deflation that accompanied the growth of capitalism relate more directly to the cycles of war and peace than to the “systemic cycles of accumulation” underlying capitalist growth. We take this point here: that the relatively higher rate of inflation and monetary expansion, after the long deflationary stretch of the last three decades, is a marker for disorder rather than a harbinger of expansion.

The end of hegemony

Where we break is in stressing that this disorder is sufficiently great as to shatter Arrighi’s notion, adapted from Fernand Braudel, that successive cycles of capitalism have meant “world capitalism… prospering, not by thrusting its roots more deeply into the lower layers of material life and market economy, but by pulling them out.”[xix] The exact opposite process is now in train: all parts of the capitalist economy are being forced, deeper and deeper into a closer relationship, with Braudel’s “lower layers” of “material life”, in two dimensions: first, the search for new value, as older lines of accumulation are blocked, is compelling capital in general to push further into zones of biological and social life otherwise outside of its circuits of accumulation – genomics, for example, or the immense social data processing industry that is Big Tech[xx] - second, and related to that blocking, the rising costs of environmental disorder and shortage are compelling greater and greater expenditures either for new raw materials or to manage the consequences of their previous use.

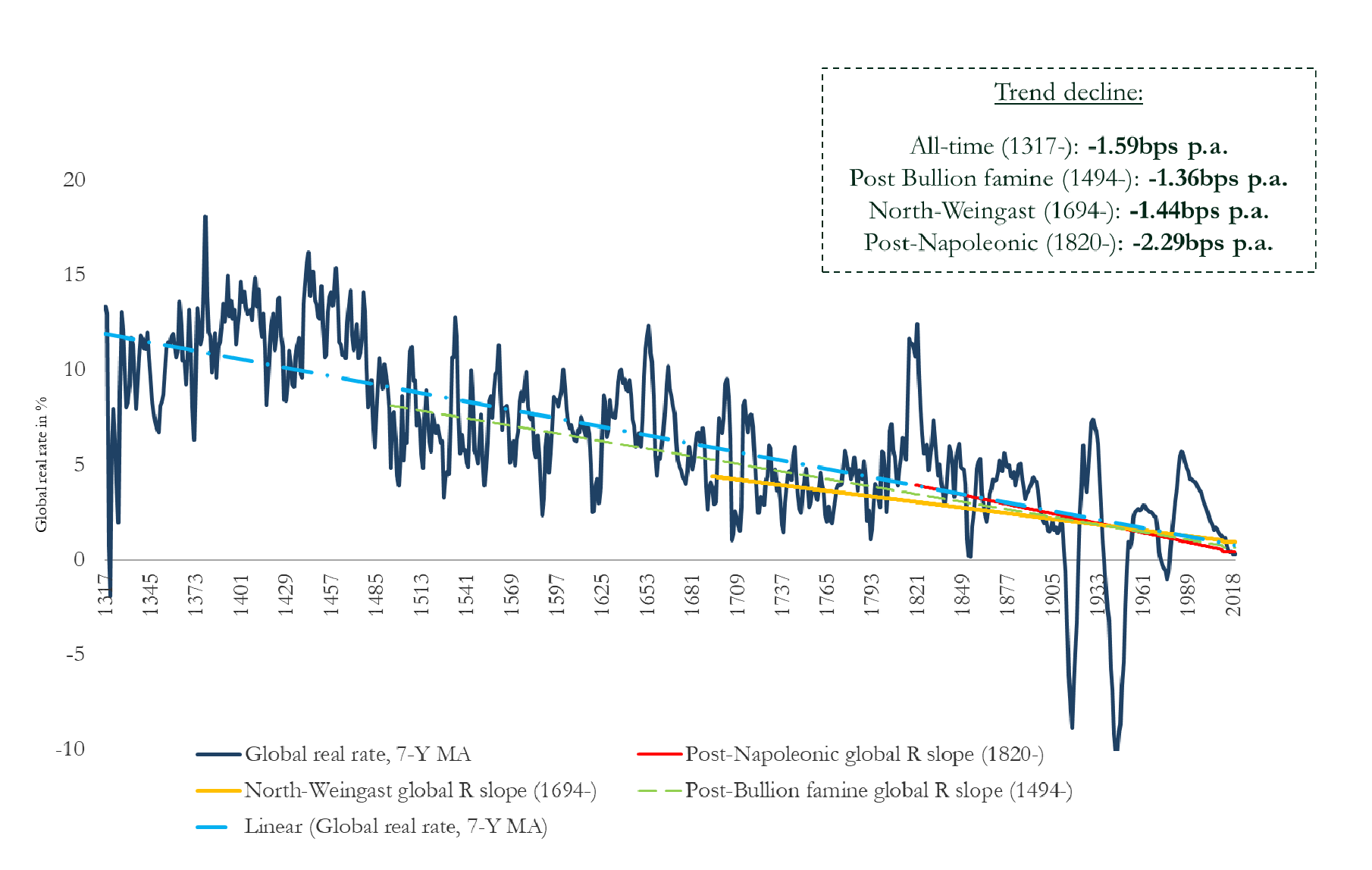

Taken together, this suggests that the “supra-secular” decline the real rate of interest of the leading capitalist economy, observable from the 1300s and functioning as the expression of the extent to which finance could “pull out” from the “roots” of material life, is coming to an end. The point at which the circulation of finance capital, and its relentless self-expansion, are conditioned by the ecological crisis is the point at which its seeming autonomy is coming to an end. Former Governor of the Bank of England, Mark Carney, is amongst those who have highlighted the grave risks to financial stability from the environmental breakdown; that grave risk, other things being equal, should translate into persistently higher real rates of interest.

Headline global real rate of interest, 1317-2018

Source: Paul Shcmelzer, January 2020, “Eight centuries of global real interest rates, R-G, and the ‘suprasecular’ decline, 1311–2018”, Staff Working Paper 845, Bank of England, figure 4. Line go down.

Speculatively, then, we might consider that the turn upwards of interest rates, across the globe, as led by the old hegemon, is not only the temporary and managerial response to post-pandemic conditions, but is therefore also the opening moment in a fundamentally new monetary period: the point at which the abstraction of finance from its material roots, as sustained by the continual expansion of the possibilities for accumulation through circulation and production, are coming to an end.

Other, more heterodox financial institutions have suggested a similar inflection point: the Bank of International Settlements suggested as early as 2020 that, peering into the future:

“a quite different picture could emerge. In this case, we would be speaking not of inflation evolving within the current policy regime, but of a more fundamental change. Here the economic landscape would, in some respects, look like the one that materialised immediately after the Second World War. This scenario could come into being if a lengthy pandemic were to leave a much larger imprint on the economy and the political sphere. In this world, public sector debt would be much higher and the public sector’s grip on the economy much greater, while globalisation would be forced into a major retreat. As a result, labour and firms would gain much more pricing power. And governments could be tempted to keep financing costs artificially low, allowing the inflation tax to reduce the real value of their debt, possibly supported by forms of financial repression.”

Being good Austrians, they can’t see beyond government as a cause for this. The possibility that critical and fundamental barriers to accumulation may exist that underly the actions even of governments does not arise for them. Nonetheless, the basic insight is correct: that the shift in the balance of costs and risks occasioned by the pandemic, and now stretching into the disorder of climate change and the ecological shift, have inflationary consequences. And note that this is somewhat anti-Keynesian: Keynes’ broad prediction, of an interest rate that would tend to zero as capital accumulated, following his hypothesis of a declining “Marginal Efficiency of Capital”, is directly challenged by the implication of a potentially long-run rising real rate of interest. The prediction here, instead, is that interest rates would trend upwards precisely because of prior capital accumulation: that continual presence of rising costs and weakening accumulation would drive the financial system, over time, in the opposite direction.

I’ve started a weekly podcast, Macrodose, broadly with the aim of applying, in a more immediate and responsive manner, the analysis being developed here. It’s a quick, 15 minute guide to (usually) the top three economics stories that week, with an environmental bent. You can find a link here, or wherever you get your podcasts (as they say).

Thought these two, parallel accounts of the physical barriers to semiconductor production were worth reading - one about Arizona, where the Biden administration is investing heavily in a new fabrication lab, and the other covering China in general. In both cases the hard constraints on water access are becoming apparent, and are set to become increasingly challenging. And semiconductor production uses crazy amounts of water: “A semiconductor plant (known as a fab) typically requires about five million gallons per day, and ten million for large foundries, equivalent to the consumption rate of 300,000 households.”

[i] The “Engels Pause” in English working-class living standards is amongst the most dramatic examples here. Robert C. Allen, "Engels' pause: Technical change, capital accumulation, and inequality in the British Industrial Revolution", Explorations in Economic History 46:4, 2009.

[ii] Alan Milward, The European Rescue of the Nation-state, London: Routledge (2nd ed.), 1999.

[iii] Salar Mohandesi and Emma Teitelman, “Without reserves” in Tithi Bhattacharya, ed., Social Reproduction Theory: Remapping Class, Recentering Oppression, London: Pluto, 2017.

[iv] Charles Goodhart, Manoj Pradhan, The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, London: Palgrave Macmillan, 2020.

[v] David P. Fidler, “SARS: Political Pathology of the first post-Westphalian pathogen” Journal of Law and Medical Ethics 31: 4, Winter 2003.

[vi] David Harvey, A Brief History of Neoliberalism, Oxford: Oxford University Press, 2005.

[vii] Adam Tooze, Shutdown: how covid shook the world’s economy, Viking: New York, 2021.

[viii] Giovanni Arrighi, The Long Twentieth Century, London: Verso, 1994.

[ix] Gürkan Çapar, “Global regulatory competition on digital rights and data protection: A novel and contractive form of Eurocentrism?” Global Constitutionalism, 2022; Nigel Cory and Luke Dasoli, “How cross-border barriers to digital trade are spreading globally, what they cost, and how to stop them”, Information Technology and Innovation Foundation, 19 July 2021 indicates that the “number of data-localization measures in force around the world has more than doubled in four years. In 2017, 35 countries had implemented 67 such barriers. Now, 62 countries have imposed 144 restrictions”.

[x] Geoff Mann, Joel Wainwright, Climate Leviathan: A Political Theory of Our Planetary Future, London: Verso, 2018.

[xi] For a critique of “socialist geoengineering”, see Drew Pendergrass and Troy Vetesse, Half-Earth Socialism, London: Verso, 2021.

[xii] For a summary, see Deborah Brown, Amos Toh, “Technology is enabling surveillance, inequality during the pandemic”, press release, Human Rights Watch, 4 March 2021. https://www.hrw.org/news/2021/03/04/technology-enabling-surveillance-inequality-during-pandemic

[xiii] Aaron Bastani, Fully Automated Luxury Communism, London: Verso, 2018.

[xiv] V.I. Lenin, The State and Revolution, Marxist Internet Archive, 1917, ch.4.

[xv] Charles Tilly, Big Structures, Huge Processes, Large Comparisons, New York: Russell Sage Foundation, 1989.

[xvi] George Labridnis, “The forms of world money”, Research in Money and Finance Discussion Paper 45, May 2014.

[xvii] Zoltan Poszar, “Bretton Woods III”, research note, Credit Suisse, 20 March 2022; James Meadway, “Bretton Woods III”, Pandemic Capitalism, blog, 27 March 2022.

[xviii] Giovanni Arrighi, The Long Twentieth Century, London: Verso, 1994, p.174

[xix] Giovanni Arrighi, The Long Twentieth Century, London: Verso, 1994, p.24

[xx] This is Rosa Luxemburg’s crucial insight in The Accumulation of Capital.